₹60,000 की salary छोड़कर freelancing शुरू करने वाले एक दोस्त ने मुझसे कहा था — “पहले महीने ₹80,000 कमाए। Job से ₹20,000 ज्यादा। बढ़िया decision था।”

छह महीने बाद उसी दोस्त ने कहा — “पता नहीं यार, हाथ में पैसा कम क्यों लग रहा है। काम ज्यादा है, income भी ज्यादा है, लेकिन financially somehow worse feel होता है।”

वो ₹80,000 कमा रहा था। लेकिन actually compare करने पर वो पुरानी ₹60,000 की salary से financially बदतर position में था।

कैसे?

क्योंकि उसने वो 5 calculations कभी नहीं कीं जो freelancing की “real” income बताती हैं। वो calculations जो किसी offer letter में नहीं होतीं, किसी YouTube video में नहीं होतीं, और ज्यादातर CAs भी tab ही बताते हैं जब tax filing का time आता है — तब तक बहुत देर हो चुकी होती है। आज के आर्टिकल में हम उसके बारे में ही चर्चा करेंगे |

Table of Contents

Calculation 1: EPF का वो ₹43,200 जो आप हमेशा के लिए छोड़ रहे हैं

यह सबसे बड़ा hidden cost है जो कोई नहीं बताता।

Salaried job में EPF दो हिस्सों से बनता है।

आपका contribution: basic salary का 12%।

Employer का contribution: basic salary का 12%।

इनमें से employer का पूरा contribution आपकी pocket से नहीं जाता,वो company देती है, ऊपर से, यह नियम होता है हमारें देश में|

मान लीजिए आपकी salary ₹60,000/month है और basic pay ₹30,000 है।

Employer EPF contribution: ₹30,000 × 12% = ₹3,600/month

साल में: ₹3,600 × 12 = ₹43,200

यह ₹43,200 आपके EPF account में जाता था ,जो आपकी सुनते-सुनते retirement corpus बन रहा था। इस पर currently EPF interest rate 8.25% है (EPFO, 2024-25)। Freelancing में यह पूरा amount आपको खुद भरना होगा,या छोड़ना होगा। अधिकांश freelancers छोड़ते ही हैं।

असली calculation यह है कि अगर आप 30 साल की उम्र में freelancing शुरू करते हैं और यह ₹43,200/year का gap 25 साल तक रहता है, तो 8% return assumption पर यह approximately ₹32-35 लाख का retirement corpus gap बनता है।

Calculation 2: Health Insurance का वो Bill जो Job में Zero था

Job में group health insurance था। ₹3-5 लाख का cover। Premium: ₹0 (company भरती थी)।

Freelancing में आप individual हैं। Market rate क्या है?

एक 28-30 साल के healthy individual के लिए ₹5 लाख का basic health insurance plan:

Public sector insurers (National Insurance, New India Assurance): लगभग ₹8,000-12,000/year Private sector (Niva Bupa, HDFC ERGO, Star Health): ₹12,000-18,000/year Super top-up plans (अगर ₹10 लाख+ coverage चाहिए): अलग से ₹4,000-8,000/year

Conservative estimate: एक decent individual health plan — ₹15,000/year।

लेकिन यह सिर्फ आपके लिए है। अगर आपकी family dependent है, spouse, बच्चे, aging parents — तो यह cost ₹40,000-80,000/year तक जा सकती है।

Job में यह benefit था। Freelancing में यह expense है।

Monthly में convert करें: ₹15,000 ÷ 12 = ₹1,250/month (सिर्फ आपके लिए)

यह directly आपकी freelancing income से कटता है — mentally भी, actually भी।

एक और layer: Job में अगर hospitalization होती थी, तो company insurance cover करती थी और आपकी salary continue रहती थी। Freelancing में hospitalization = no work = no income + hospital bills। इसका कोई exact number नहीं है, लेकिन यह risk real है।

Calculation 3: Irregular Income का Emergency Fund — जो 3 Months नहीं, 9 Months होना चाहिए

“3 months का emergency fund रखो।” यह advice सुनी होगी।

यह advice salaried employees के लिए है। Freelancers के लिए यह dangerous रूप से कम है।

एक salaried person के साथ worst case: नौकरी जाती है, 1-3 महीने में नई मिलती है। Income gap maximum 3 months।

एक freelancer के साथ worst case: तीन बड़े clients एक साथ project pause करते हैं (यह 2020 में हजारों freelancers के साथ हुआ था)। नए clients build करने में 3-6 महीने। Total income gap: 6-9 months।

इसके अलावा freelancing income naturally irregular होती है। January में ₹1.2 लाख, February में ₹40,000, March में ₹90,000। Average अच्छा है — लेकिन February में EMI, rent, और insurance premium सब आते हैं।

Freelancer का emergency fund formula-

अपना average monthly expense calculate करिए — rent, groceries, utilities, insurance, loan EMIs, सब मिलाकर। इसे 9 से multiply करिए।

अगर monthly expenses ₹35,000 हैं: ₹35,000 × 9 = ₹3,15,000

यह आपका minimum freelancing emergency fund है।

यह बड़ा लगता है। और है भी। लेकिन इसे liquid रखिए — savings account नहीं, liquid mutual fund या short-term FD। HDFC Liquid Fund, SBI Liquid Fund जैसे options में roughly 6-7% return मिलता है (historical average, guaranteed नहीं), और 1-2 business days में withdrawal।

Freelancing शुरू करने का सबसे practical advice: Job छोड़ने से पहले यह emergency fund build करिए। Job में रहते हुए। Side income से। Slowly। यह fund ready होने के बाद ही full-time freelancing का jump लीजिए।

Calculation 4: Section 44ADA का Tax — जो “Low” लगता है लेकिन है नहीं

यह calculation सबसे confusing है और सबसे ज्यादा लोग यहाँ गलती करते हैं।

Freelancers और professionals के लिए Section 44ADA of Income Tax Act, 1961 एक presumptive taxation scheme है। इसमें आपको detailed accounts maintain नहीं करने होते। Gross receipts का 50% automatically “profit” मान लिया जाता है, और उसी पर tax लगता है।यह applicable है: doctors, lawyers, engineers, architects, accountants, technical consultants, interior decorators — और generally “specified professions” के लिए। IT freelancers, content writers, designers — इनके लिए applicability case-by-case होती है। अपने CA से confirm करिए।

Actual math इसका यह है कि Annual freelancing income: ₹12 लाख Section 44ADA presumptive profit (50%): ₹6 लाख Basic exemption limit (new tax regime, FY 2024-25): ₹3 लाख Taxable income: ₹3 लाख

Tax at 5% (₹3-7 lakh slab, new regime): ₹15,000

- Health & Education Cess (4%): ₹600 Total tax: ₹15,600

अगर आपकी annual tax liability ₹10,000 से ज्यादा है, तो आपको advance tax भरना होगा,quarterly। June 15, September 15, December 15, March 15। अगर नहीं भरा, तो Section 234B और 234C under Income Tax Act के under interest penalty लगती है।

बहुत से नए freelancers को यह पहले साल पता नहीं होता। Tax filing के वक्त tax तो भरते हैं, साथ में interest penalty भी देनी पड़ती है।

Calculation 5: Gratuity का वो ₹1-3 लाख जो हमेशा के लिए गया

यह सबसे “invisible” calculation है। Payment of Gratuity Act, 1972 के under, अगर आपने एक company में 5 साल continuous service complete की है, तो आप gratuity के eligible हैं।

Formula: (Last drawn salary × 15 × years of service) ÷ 26

Example: ₹60,000 salary × 15 × 6 years ÷ 26 = ₹2,07,692

यह ₹2 लाख+ आपको 5 साल की service पर automatically मिलते, बिना किसी extra investment के, purely tenure के reward के रूप में।

Freelancing में यह exist नहीं करता। कोई आप किसी कंपनी में काम करते ही नहीं है, आप अपना काम खुद करते हैं, और यह calculation और complicated होती है अगर आप 3-4 साल की service पर job छोड़ रहे हैं। 5 साल पूरे नहीं हुए — gratuity zero।

इसका मतलब यह नहीं कि job मत छोड़िए। लेकिन अगर आप 3.5 साल की service पर हैं और freelancing का plan है — 5 साल तक रुककर gratuity collect करने का financial sense हो सकता है। यह strictly personal decision है, लेकिन calculation करके decision लीजिए।

तो Freelancing के लिए “Breakeven” Salary कितनी होनी चाहिए?

यह article का सबसे practical section है।

अगर आपकी current salary ₹60,000/month है, तो freelancing में आपको कितना कमाना होगा ताकि आप actually equal हों?

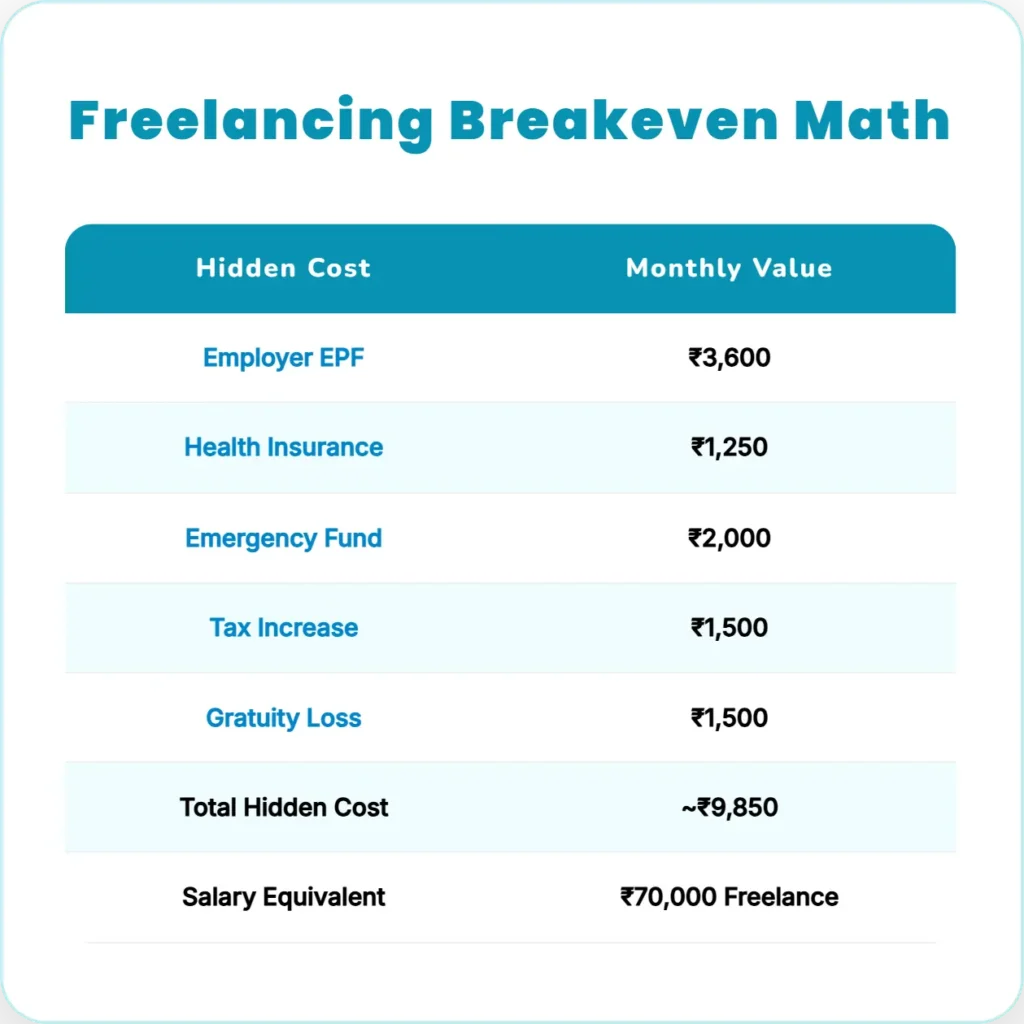

| छूटने वाला benefit | Monthly equivalent |

| Employer EPF contribution | ₹3,600 |

| Health insurance premium | ₹1,250 |

| Emergency fund building (extra 6 months) | ₹2,000 (amortized) |

| Tax increase (advance tax + compliance cost) | ₹1,500 (estimate) |

| Gratuity loss (amortized) | ₹1,500 |

| Total hidden cost | ~₹9,850/month |

यानी ₹60,000 की salary replace करने के लिए freelancing में roughly ₹70,000/month चाहिए — सिर्फ breakeven के लिए। Growth, lifestyle upgrade, और investment के लिए इससे ऊपर।

यह calculation आपकी specific situation में अलग होगी। Numbers change होंगे। लेकिन direction यही रहेगा।

इस article में mention किए सभी figures — EPF rates, tax slabs, insurance premiums — March 2026 तक की publicly available information पर based हैं। Tax laws change होते हैं, insurance premiums age और health के साथ vary करते हैं। Freelancing decision लेने से पहले एक qualified CA से अपनी specific situation discuss करिए।

यह article आपको सही questions पूछना सिखाने के लिए है,सभी answers देने के लिए नहीं।

अंत में मैं यही बोलूँगा कि Freelancing एक genuinely अच्छा career path हो सकता है। लेकिन वो decision informed होनी चाहिए।